Endnote

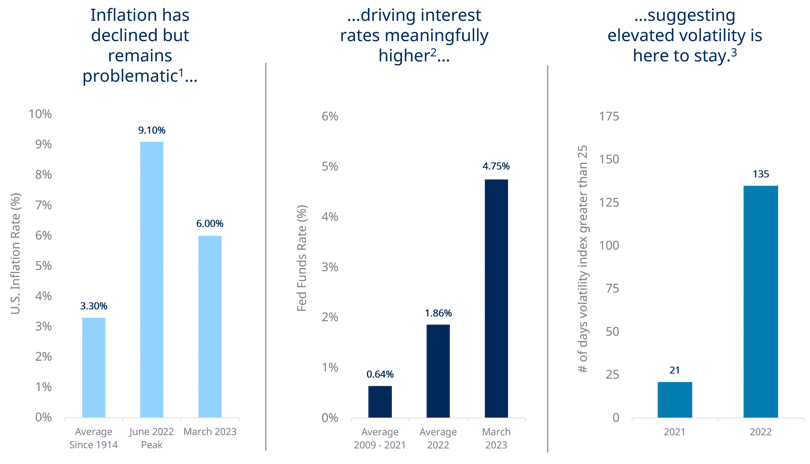

- Bloomberg as of March 1, 2023. Historical average inflation rate represented by all inflation data since reporting began in 1914. Recent peak as of June 30, 2022.

- Bloomberg as of March 1, 2023. Based on upper-bound of the median consensus estimates (Fed Dots) of the Federal Funds Target Rate.

- Bloomberg, S&P Global Market Intelligence as of December 31, 2022. Volatility is measured by the “VIX” which is the Chicago Board Options Exchange Volatility Index. It is designed to be a real-time estimate of the expected volatility of the S&P 500 and is calculated using the mid-point of S&P 500 (SPX) option bid/ask quotes.

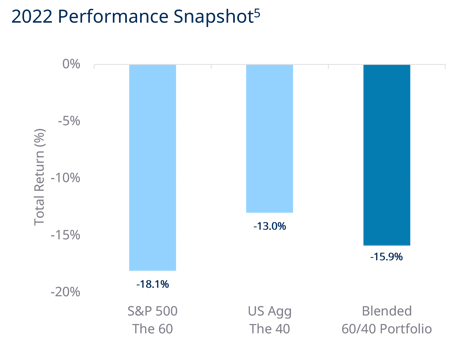

- Bloomberg as of December 31, 2022. A hypothetical portfolio consisting of 60% equities represented by S&P 500 and 40% bonds represented by U.S. Aggregate Bond Index returned -16.9%.

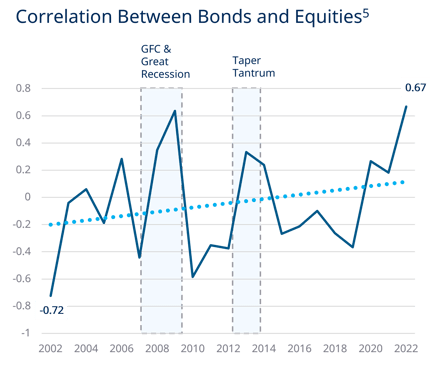

- Bloomberg as of December 31, 2022. Bonds represented by U.S. Aggregate Bond Index, Equities represented by S&P 500.

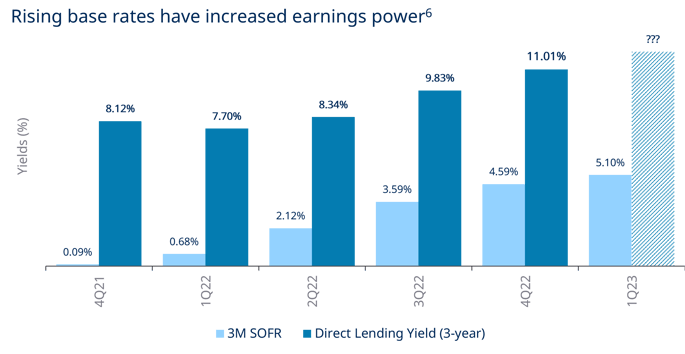

- Cliffwater. “Direct Lending” represented by the Cliffwater Direct Lending Index (CDLI) as of September 30, 2022; Bloomberg. 3-month term SOFR (ticker: TSFR3M Index) as of 03/09/2023.

- Fitch Ratings Ultimate Recovery Rate Study, March 2022.

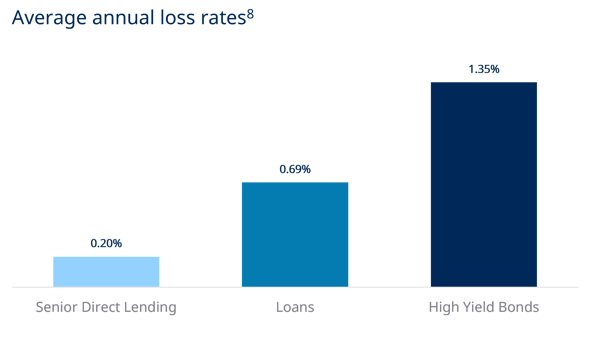

- Average annual loss rates since data for Cliffwater Direct Lending Senior Index began in 2011. Source: SP LCD, Cliffwater, JP Morgan. Market loss rates calculated as average loss rates and defined as: for loans, based on SP LCD default rates for all loan $ defaults as percentage of total outstanding and calculated as default*(1 – average historical Recovery Rate) from 2011 to December 2022; Direct Lending based on Cliffwater Direct Lending Senior Index realized gains/losses from 2011 to December 2022; High Yield Bonds based on JP Morgan Default Monitor annual defaults and calculated as default* (1 – average historical Recovery Rate) from 2011 to December 2022; Recovery rates for loans of range from 48-63% by year and 22-55% for bonds and are based on JP Morgan Default Monitor, February 1, 2022.

- Cliffwater. “Direct Lending” represented by the Cliffwater Direct Lending Index (CDLI), High Yield represented by the Bloomberg Barclays US Corporate High Yield Index, Traded Loans represented by the S&P/LSTA Leveraged Loan Index.

- Cliffwater. “Direct Lending” represented by the Cliffwater Direct Lending Index (CDLI) as of September 30, 2022; Bloomberg: “Equities” represented by the S&P 500 as of September 30, 2022.

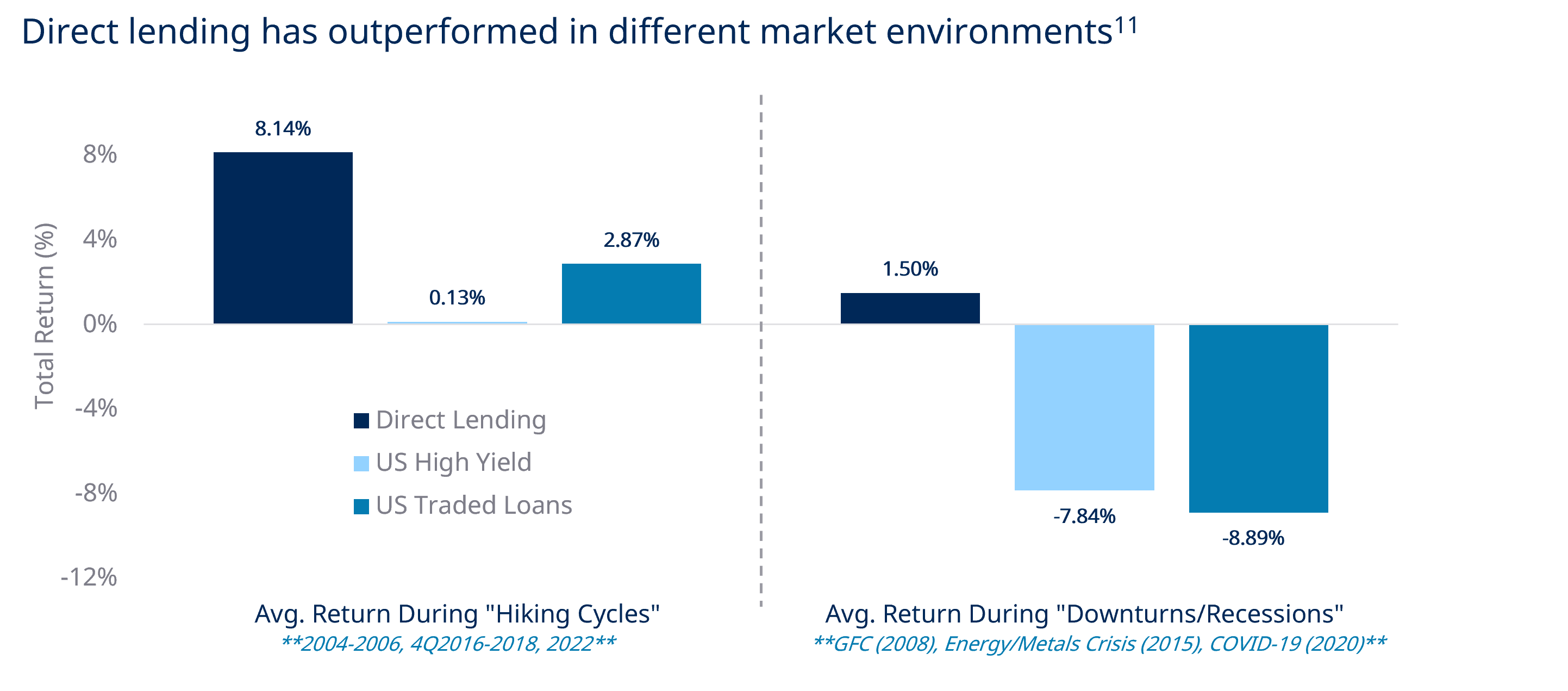

- Data as of December 31, 2022 unless otherwise noted. Sources: “US Traded Loans” represented by the Morningstar LSTA Leveraged Loan Index, “US High Yield” represented by Bloomberg Barclays US High Yield Index, and “US IG Credit” represented the Bloomberg Barclays US Corporate Bond Index. “Direct Lending” represented by the Cliffwater Direct Lending Index as of 09/30/2022.

- Preqin Investor Outlook: Alternative Assets H1 2023.

Important information

Unless otherwise indicated, the Report Date referenced herein is March 31, 2023. Past performance is not a guarantee of future results.

The material presented is proprietary information regarding Blue Owl Capital Inc. (“Blue Owl”), its affiliates and investment program, funds sponsored by Blue Owl, including the Blue Owl Credit, GP Strategic Capital Funds and the Real Estate Funds (collectively the “Blue Owl Funds”) as well as investment held by the Blue Owl Funds.

The views expressed and, except as otherwise indicated, the information provided are as of the report date and are subject to change, update, revision, verification, and amendment, materially or otherwise, without notice, as market or other conditions change. Since these conditions can change frequently, there can be no assurance that the trends described herein will continue or that any forecasts are accurate. In addition, certain of the statements contained in this webpage may be statements of future expectations and other forward-looking statements that are based on the current views and assumptions of Blue Owl and involve known and unknown risks and uncertainties (including those discussed below) that could cause actual results, performance, or events to differ materially from those expressed or implied in such statements. These statements may be forward-looking by reason of context or identified by words such as “may, will, should, expects, plans, intends, anticipates, believes, estimates, predicts, potential or continue” and other similar expressions. Neither Blue Owl, its affiliates, nor any of Blue Owl’s or its affiliates’ respective advisers, members, directors, officers, partners, agents, representatives or employees or any other person (collectively the “Blue Owl Entities”) is under any obligation to update or keep current the information contained in this document.

This webpage contains information from third party sources which Blue Owl has not verified. No representation or warranty, express or implied, is given by or on behalf of the Blue Owl Entities as to the accuracy, fairness, correctness or completeness of the information or opinions contained in this webpage and no liability whatsoever (in negligence or otherwise) is accepted by the Blue Owl Entities for any loss howsoever arising, directly or indirectly, from any use of this webpage or its contents, or otherwise arising in connection therewith.

Benchmark definitions

S&P 500 Index: A stock market index that measures the stock performance of 500 large companies listed on stock exchanges in the United States.

10-Year Treasury: The 10-year Treasury note is a debt obligation issued by the United States government with a maturity of 10 years upon initial issuance. A 10-year Treasury note pays interest at a fixed rate once every six months and pays the face value to the holder at maturity.

U.S. Aggregate represented by the Bloomberg Barclays US Aggregate Bond Index. This index is a broad-based flagship benchmark that measures the investment grade, US dollar-denominated, fixed-rate taxable bond market. The index includes Treasuries, government-related and corporate securities, mortgage-backed securities, asset backed securities and commercial mortgaged backed securities.

Corp. Investment Grade represented by the Bloomberg Barclays U.S. Corporate Bond Index. This Index measures the investment grade, fixed-rate, taxable corporate bond market. It includes USD-denominated securities publicly issued by US and non-US industrial, utility, and financial issuers.

Corp. High Yield represented by the Bloomberg Barclays US Corporate High Yield Index. This index measures the USD- denominated, high yield, fixed-rate corporate bond market.

Leveraged Loans represented by the S&P/LSTA Leveraged Loan Index. This Index is a common benchmark and represents the 100 largest and most liquid issues of the institutional loan universe.

Direct lending represented by the Cliffwater Direct Lending Index (CDLI). The CDLI seeks to measure the unlevered, gross of fee performance of U.S. middle market corporate loans, as represented by the asset-weighted performance of the underlying assets of Business Development Companies (BDCs), Including both exchange-traded and unlisted BDCs, subject to certain eligibility requirements.

All investments are subject to risk, including the loss of the principal amount invested.

These risks may include limited operating history, uncertain distributions, inconsistent valuation of the portfolio, changing interest rates, leveraging of assets, reliance on the investment advisor, potential conflicts of interest, payment of substantial fees to the investment advisor and the dealer manager, potential illiquidity, and liquidation at more or less than the original amount invested. Diversification will not guarantee profitability or protection against loss. Performance may be volatile, and the NAV may fluctuate.

This webpage is for informational purposes only and is not an offer or a solicitation to sell or subscribe for any fund and does not constitute investment, legal, regulatory, business, tax, financial, accounting, or other advice or a recommendation regarding any securities of Blue Owl, of any fund or vehicle managed by Blue Owl, or of any other issuer of securities. Only a definitive offering document (i.e.: Prospectus or Private Placement Memorandum) can make such an offer.

5538539