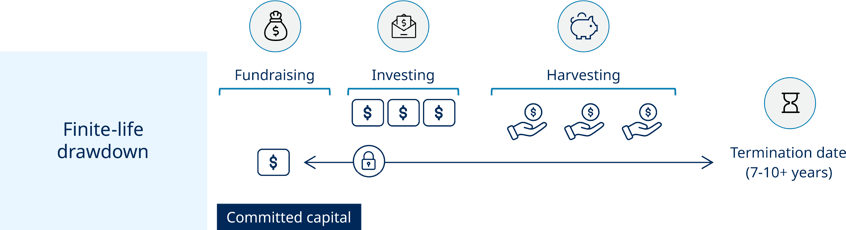

Unlike typical public-market funds, drawdown vehicles don’t immediately invest all funds. Instead, investors commit a specified amount of capital upfront.

Then, throughout the fund’s initial investment period, the fund manager issues “capital calls” to investors, gradually deploying their commitments into targeted investments.

In the interim, undeployed capital is typically held—at the investor’s discretion—in a mix of cash, cash equivalents, bonds, and public equities, depending on individual preferences and portfolio strategy.

Drawdown funds generally have a defined lifecycle (e.g., ten years) with potential extensions to facilitate exits and fully realize returns3. This structure is common in private equity, venture capital, and other alternative strategies for patient, long-term capital.

For illustrative purposes only. Actual fund features, including subscription, redemption, and reinvestment policies, may vary and are subject to fund-specific offering documents and market conditions. There is no guarantee of immediate capital deployment, reinvestment of proceeds, or availability of liquidity windows.

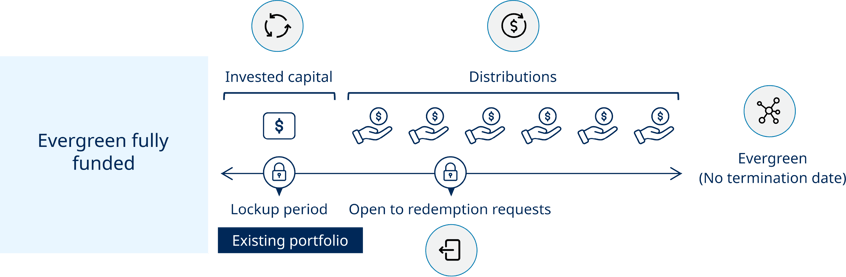

Unlike drawdown funds, evergreen vehicles do not have a fixed end date. Instead, they typically allow investors to subscribe at regular intervals, subject to limitations. Capital is often deployed immediately into a diversified portfolio of private assets.

While distributions of income may be delivered throughout, as investments generate returns or are exited, proceeds are typically reinvested rather than distributed—helping maintain consistent exposure and support compounding potential.

These funds typically offer periodic redemption windows—often quarterly—subject to liquidity constraints (e.g., up to 5% of net assets).

Evergreen funds are increasingly used across private equity, credit, and real asset strategies, offering a streamlined way to access private markets with reduced operational complexity and improved liquidity features.

For illustrative purposes only. Actual fund features, including subscription, redemption, and reinvestment policies, may vary and are subject to fund-specific offering documents and market conditions. There is no guarantee of immediate capital deployment, reinvestment of proceeds, or availability of liquidity windows.

| Category | Drawdown fund | Evergreen fund |

|---|---|---|

| Cell label Capital commitment & deployment | Cell label Investors commit capital upfront; deployed gradually via capital calls over time | Cell label Immediate deployment upon investment; capital is continuously raised and reinvested |

| Cell label Fund lifecycle & structure | Cell label Fixed term (typically ~10 years); structured entry and exit periods | Cell label Indefinite, open-ended structure with no set end date |

| Cell label Liquidity & redemption | Cell label Illiquid until investments are exited or mature; liquidity events planned | Cell label Periodic redemption windows (e.g., quarterly); up to 5% of NAV may be redeemed, subject to terms |

| Cell label Investment proceeds | Cell label Realized proceeds are distributed to investors | Cell label Proceeds are reinvested into new opportunities, maintaining portfolio exposure |

| Cell label Transparency & reporting | Cell label Less frequent NAV updates; valuations may be opaque between reporting periods | Cell label Frequent NAV reporting (monthly or quarterly); enhanced transparency due to SEC oversight |

| Cell label Tax documentation | Cell label Investors receive Schedule K-1 | Cell label Investors typically receive Form 1099 |

| Cell label Exit strategy | Cell label Defined exit strategy (e.g., IPO, sale, recapitalization) aligned with fund term | Cell label No predefined exit; investors can enter/exit more flexibly over time |

| Cell label Investor appeal | Cell label Suited for long-term, illiquid commitments with structured timelines | Cell label Appeals to investors seeking flexible, streamlined access to private markets |

While traditional drawdown funds are designed to target strong absolute returns, their staged capital deployment can lead to periods of idle capital—commonly referred to as “cash drag.” In contrast, evergreen funds deploy capital immediately and continuously, which can help accelerate compounding and improve overall return efficiency.

Rather than viewing these structures as either/or, many advisors are now combining them. Evergreen funds can serve as a core allocation, offering the potential for steady exposure, reinvestment of distributions, and liquidity flexibility. Meanwhile, drawdown funds can act as satellite positions, providing targeted access to specific managers, strategies, or vintages.

Drawdown funds: Satellite positions providing targeted access to specific managers, strategies, or vintages.

Evergreen funds: Core allocation, Offering the potential for steady exposure, reinvestment of distributions, and liquidity flexibility

For illustrative purposes only. Portfolio construction decisions, including the role of evergreen or drawdown strategies, should be based on each investor’s individual circumstances and objectives.

Together, they can help reduce reinvestment risk, smooth capital deployment, and balance private markets exposure across portfolios.