Utilizing innovations in alternative investments to seek tax efficiency.

.png?width=80&height=80&name=Icon%20-%20Saver%20(40x40).png)

A young family with solid income but on a tight budget, trying to get ahead but at the same time faced with a lot of current expenses—has a lot in common with the university endowment trying to generate returns to meet complex operating budgets.

.png?width=80&height=80&name=Icon%20-%20Spender%20(40x40).png)

An older client who might have postponed prudent savings decisions and is now in catchup-mode—looks a lot like an underfunded pension in terms of the need to reach for yield.

.png?width=80&height=80&name=Icon%20-%20Grower%20(40x40).png)

A client who is ahead of the curve in terms of planning for the future, shares a lot in common with a large sovereign fund with little immediate-term liquidity pressure.

.png)

A young family with solid income but on a tight budget, trying to get ahead but at the same time faced with a lot of current expenses—has a lot in common with the university endowment trying to generate returns to meet complex operating budgets.

.png)

An older client who might have postponed prudent savings decisions and is now in catchup-mode—looks a lot like an underfunded pension in terms of the need to reach for yield.

.png)

A client who is ahead of the curve in terms of planning for the future, shares a lot in common with a large sovereign fund with little immediate-term liquidity pressure.

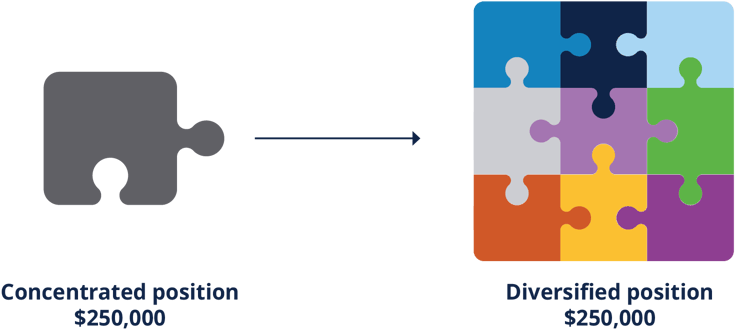

Your clients, particularly those that work for medium and large corporations, may develop concentrated equity positions in their portfolios over time, often due to equity compensation. Employee stock options, restricted stock units, or other company equity can provide growth opportunities but also increase the likelihood of an overly concentrated portfolio. These individuals likely need diversification but may face serious tax issues if they are to sell this stock. This burden is made all the more extreme by the fact that for many clients, these stocks will likely have a low cost-basis in their portfolio.

Figure 4

One potential solution to this problem may be an exchange fund. With an exchange fund, a client donates their shares to the fund and receives a portion of the fund ownership in return. They achieve diversification because now instead of holding a heavily concentrated ownership position in a single stock, they own shares of a diversified portfolio of stocks, and your clients defer capital gains tax because the transaction is structured as an exchange, rather than a sale and purchase. Exchange funds have a mandatory 7-year lockup period and are required by law to hold a certain fraction of assets in illiquid securities, so exchange funds are not right for everyone—they do not solve problems for a client with immediate liquidity needs. Nevertheless, they can be a useful tool for providing a client with increased diversification without triggering tax liability.

Many of your clients are not just invested in public and private capital markets, they own specific pieces of real estate, like business properties, rental homes, land and other “real properties”. Selling a property of this nature can generate a significant tax burden if it is not managed correctly. Fortunately, an IRC Section 1031 exchange (a “1031 exchange”) provides a way to potentially defer the tax burden from real estate sales.

In a 1031 exchange, a person selling a qualifying real estate investment can reinvest some or all of the proceeds in qualifying “like kind” replacement property, potentially deferring tax liability on the return. In principle, this is somewhat similar to the logic that applies when a person sells their primary home and buys another home; some or all of the profits they made on the sale of their primary home may be protected from tax liability because they are rolled over into the new home purchase. A 1031 exchange can achieve a similar outcome from a tax deferral standpoint. Taxpayers can acquire replacement real estate investments directly or potentially acquire interests in carefully structured tax-advantaged investment vehicles to complete their own 1031 exchange.

A simple numerical example illustrates the power of a 1031 exchange. Consider an individual who sold a vacation home for $1m. They bought this home for $500,000 and have taken $300,000 of corresponding depreciation deductions by the time of sale. Because the adjusted tax basis of the house is $200,000, the individual now owes tax on their $800,000 gain. If subject to federal income tax at 20%, this can take up to $160,000 away to pay applicable taxes. However, the individual may also owe state, local, and other taxes (such as the Net Investment Income Tax), depending on their individual circumstances and jurisdiction. These additional taxes could amount to another $160,000 or more. The after-tax proceeds of the sale could likely amount to $680,000 if there were no tax deferral, depending on the tax jurisdiction.

Now suppose that before the sale of the property, the individual had arranged with a “qualified intermediary” -- an independent facilitator of 1031 exchanges allowed by applicable tax rules, typically associated with a title company, a real estate attorney, or in some cases a bank -- to enter into a 1031 exchange rather than selling the property directly. Instead of the individual receiving the proceeds of the sale, the proceeds go into escrow with the qualified intermediary and are then transferred into the purchase of another qualified real estate investment. If done properly, this can defer tax liability on the sale of the property.

Engaging in a 1031 exchange takes advanced planning and careful compliance with all applicable tax rules. Generally, if your client takes receipt of the proceeds of the sale (either directly or indirectly, e.g., through an agent), it is too late to engage in a 1031 exchange. Other rules, including the impact of leverage and the number of replacement properties, may also affect the viability of a 1031 exchange. But helping your client plan in advance, including finding the right qualified intermediary, can be a powerful way to assist them when it comes time to make major adjustments to a personal estate such as this.