|

GP/LP (Alts 1.0) |

Evergreen funds (Alts 2.0) |

Mutual funds |

|

|---|---|---|---|

|

Cell label

Structure |

Cell label

Closed-end, limited partnership |

Cell label

Open-end |

Cell label

Open-end |

|

Cell label

Investor eligibility |

Cell label

Varies, may include Qualified Purchasers and Accredited Investors depending on structure |

Cell label

Varies, may include Accredited and non-accredited investors depending on structure |

Cell label

Any investor |

|

Cell label

Investment minimum |

Cell label

Varies, typically starting at $5 million |

Cell label

Varies; evolving access points rather than fixed minimums |

Cell label

Varies; evolving access points rather than fixed minimums |

|

Cell label

Pricing |

Cell label

Quarterly |

Cell label

Typically quarterly or monthly NAV/pricing |

Cell label

Daily |

|

Cell label

Performance reporting |

Cell label

Closed-end, limited partnership |

Cell label

Typically quarterly or monthly |

Cell label

Typically quarterly or monthly |

|

Cell label

Capital deployment / funding |

Cell label

Multi-year commitment |

Cell label

Immediate deployment upon investment |

Cell label

Immediate deployment upon investment |

|

Cell label

Liquidity |

Cell label

None, typically 10-year lock-up period |

Cell label

Periodic, typically quarterly and subject to gates, notice periods, or other limits (may vary by product) |

Cell label

Daily |

|

Cell label

Tax reporting |

Cell label

K-1 |

Cell label

1099 |

Cell label

1099 |

|

Cell label

Fund life |

Cell label

Typically, 10 or more years |

Cell label

Indefinite |

Cell label

Indefinite |

Past performance is not indicative of future results. There can be no assurance that historical trends will continue.

For illustrative purposes only. Features may vary by products and are not representative of any specific investment offering. This information is not intended as a recommendation or endorsement of any particular investment type

The liquidity of alternative strategies, like any investment, has two dimensions: the liquidity of the underlying assets in which the strategy invests and the liquidity terms of the vehicle structure itself.

Private assets are illiquid in nature. They not only have longer investment horizons in order to maximize value creation but are also subject to different transaction dynamics — selling a stake in a private company or property may involve negotiations that can take months to close. Consequently, investor capital is not readily accessible in a traditional private fund. Evergreen funds, on the other hand, make it possible for individuals to invest in illiquid assets while offering periodic liquidity features, subject to the structure’s parameters.

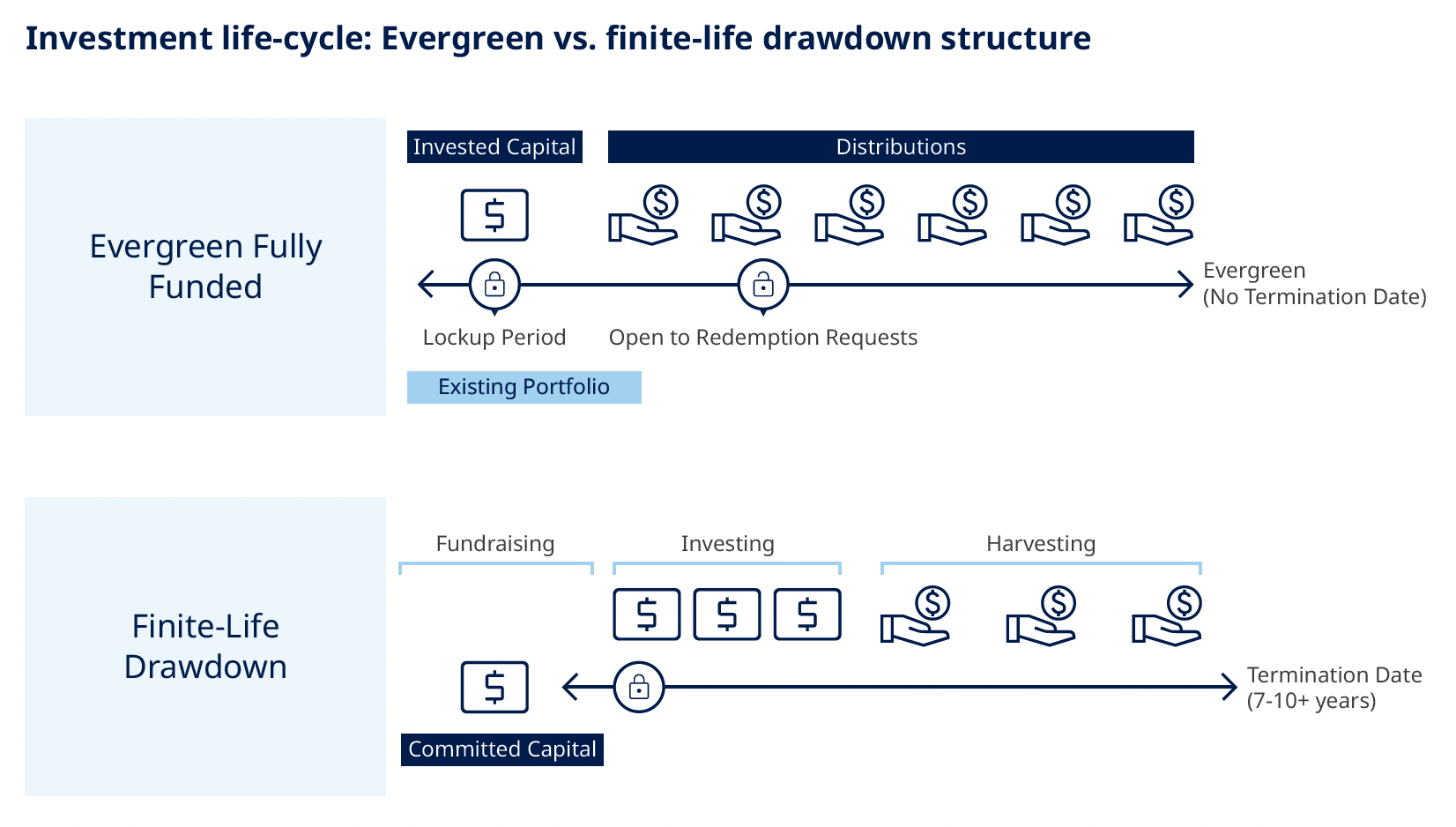

For illustrative purposes only. This comparison is a conceptual summary and may not reflect the precise characteristics, liquidity features, or timelines of any particular evergreen or drawdown structure. Actual structures vary.

When considering allocations to private markets, investors should weigh trading off daily liquidity in exchange for the potential of enhanced returns and reduced volatility. Many investors, particularly those with longer time horizons, may find that they do not require their portfolios to have 100% liquidity, 100% of the time.